Howard Waitzkin

A. Joseph Layon

Introduction

Barriers to access and the financial burden of health care, no longer problems in many economically developed nations, have emerged as major concerns in the United States. Over the past century, initiatives to resolve barriers to access, as well as legislative and administrative maneuvers to rein in cost, have failed. New investigative techniques in health services research, based largely on the cost-effectiveness model, have entered into the evaluation of technology and clinical practices, including those in critical care medicine. In this chapter we will place critical care in the context of the U.S. health system characterized—especially—by access and cost problems; offer an interpretation that traces problems of costs to underlying social contradictions and social structures within and outside the health system; and consider how these issues might change under varying models of a national health program.

While we provide a discussion of possible organizational and financing methods for a health system, the reader should understand that our viewpoint of a potentially optimal system is clearly expressed; while some of our colleagues will disagree with this view, we welcome the needed debate.

Barriers to Access: The Human Experience

Barriers to health care access have become pervasive in the United States. These barriers not only prevent a sizeable number of our fellow citizens from receiving needed services—the number is approximately 57 to 59 million without access (1) at some point during a year (Fig. 1.1 and Table 1.1) and 47 million (16% of our population) without access throughout the year (2,3)—but also impose fundamental ethical problems for physicians and other health workers who find themselves unable to solve problems that may lead to patients' morbidity or even mortality.

We will detail the global picture in a later section. However, below we wish to use the following summaries to depict the experiences of patients seen personally by one of us (HW), a practitioner of general internal medicine, and teacher of residents and students at community health centers and public hospitals. Although these examples do not comprehensively depict all the barriers to access that patients experience in the United States, they do give a human face to the troubling statistical data on access barriers. Some of the patients experienced problems that required critical care; others might well have required critical care if primary care practitioners had not intervened. The stories also provide a context for the policy analyses and recommendations for change that follow.

Fellow Citizens Suffering from Cutbacks and Increased Copayments under Medicaid

The first two patients illustrate problems of access for patients covered under Medicaid, the joint state–national program that aims to ensure access to care for eligible, low-income people. Medicaid covers individuals with dependent children, those who are disabled, and many people in nursing homes. To be eligible, a person must earn a monthly income falling below the level of poverty determined by state and federal governments.

· A 31-year-old diabetic and legally blind man began to experience severe unilateral headaches but could not afford a computed tomography (CT) scan of the head because his monthly deductible under Medicaid, which he was required to pay out of pocket each month, increased from $50 to $250. He later was brought delirious to the emergency room, where an emergency CT scan revealed a brain tumor with poor prognosis. After several days in the intensive care unit, he died. At his death, his physicians felt that the tumor may have been resected successfully if he had received attention earlier, when his severe headaches first began.

· A 56-year-old man with metastatic soft tissue sarcoma could not afford follow-up visits, medications, visiting nurse, or hospice, because his deductible under Medicaid had increased to $350 per month. This patient died in pain and without adequate nursing support in his home because of financial barriers.

Fellow Citizens Facing Restrictions due to Policies of a County-administered Medically Indigent Adult Program

The next group of patients did not receive needed care despite eligibility for medical benefits under the county government's program for medically indigent adults (MIAs). This program covers adults who are not eligible under the Medicaid program, but whose income is below the state-defined poverty limit. To reduce costs, many states decentralized MIA programs to county governments during the early 1980s. Counties vary widely in services provided and in copayments required from patients.

|

|

|

Figure 1.1. Estimated number of nonelderly people without health insurance at defined periods of 1998. Numbers in millions. Source: Congressional Budget Office. |

· A 63-year-old man with hypertension, renal insufficiency, and prostatic hypertrophy causing urinary obstruction could not gain approval from the county's MIA program for a prostatectomy, because it was considered an elective procedure. His urinary obstruction and renal function gradually worsened. Eventually, he was admitted to an intensive care unit with renal failure and severe hypertension. At that point, because he required dialysis, he became eligible for federal Medicare benefits. The very significant costs of dialysis—more than $100,000 per year—were likely avoidable had he been allowed to undergo the prostatectomy when initially indicated.

· A 52-year-old man developed unstable angina after a myocardial infarction, for which he was admitted to a coronary care unit. The MIA program disapproved funding for elective coronary angiography, even though national standards of cardiologic practice required its being performed under these circumstances.

Abandonment due to Inability to Pay

Many patients in the United States have established relationships with physicians who follow them for many years until, either because of job loss, a company's decision not to provide insurance as a fringe benefit, divorce or death of a spouse, geographic relocation, or other changes in circumstances, they lose their insurance. While some physicians will continue to care for a patient with whom they have an established relationship, others, at the time that their patient loses insurance, may decline to continue to follow the patient, because of the patient's inability to pay full fees. “Abandonment” is a legal principle, by which the physician is prevented from declining to see a patient whom he or she previously has followed unless a suitable substitute is arranged and the patient agrees to this arrangement (4). Nevertheless, neither governmental agencies nor professional organizations enforce these principles in cases when patients lose insurance.

|

Table 1.1 Some Consequences of Being Uninsured in the United States |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

· A 63-year-old man with hypertension, renal insufficiency, and prostatic enlargement causing urinary obstruction, described above, had worked for many years as a custodian for a small health maintenance organization (HMO). While he worked there, one of the HMO's physicians saw him informally for his high blood pressure. Because the HMO did not provide health care as a fringe benefit for its own nonprofessional employees, these visits generally were provided as a free service by the physician, who believed that an employee with a major health problem should receive at least some needed care. After a cutback, however, the HMO laid off this patient from his job, and the physician decided that he no longer could justify offering free services. As a result, the patient spent several months with severe hypertension, until he could be seen at a local community health center.

· A 44-year-old unemployed woman was followed by her physician for about 8 years because of reflex sympathetic dystrophy, a very painful condition of her legs and feet that periodically required low doses of a narcotic and a tranquilizer for symptom relief. When the patient went through a divorce, she lost her husband's insurance coverage. Shortly thereafter, her long-time physician informed her that, because she now lacked insurance, he could no longer see her. Several months passed during which she could not receive needed treatment, until a physician at a community health center agreed to see her.

Treatment Delay because of Noninsured Status and Early Death

One of the most troubling effects of access barriers in the United States involves deaths that could be prevented if people were able to obtain required care. In our experience, such tragedies arise most commonly when patients cannot find appropriate services for the diagnosis and treatment of cancer. When symptoms of cancer arise, such patients experience critical delays, with a deleterious impact on the eventual outcome of their disease. Problems in cancer services arise for patients who face access barriers despite coverage by public insurance, as noted previously. Barriers become especially grim, however, when patients lack insurance altogether.

· A 48-year-old Japanese American woman ran her own small landscape gardening business. Because of the high cost of individual health insurance policies, she decided to remain uninsured. After noticing a breast lump, she delayed seeking care because she did not have a regular doctor and because she feared the expenses of care; she hoped the mass would disappear. When the mass continued to grow after 3 months, she began to seek care from private physicians, who declined to see her due to lack of insurance. After 6 months, she eventually was able to find care at a community health center. Evaluation for metastatic disease was arranged by special request with a nuclear medicine facility at a university hospital; without the personal intervention of her physicians and the donation of specialty services, the appropriate scan would not have been done. The scan revealed extensive metastatic cancer. Her chemotherapy also was delayed because of access barriers. At one point, she was admitted to an intensive care unit with life-threatening complications of metastatic cancer. Within 6 months, the patient died.

Lack of Medical Care to the Homeless Threatening the Health of the General Community

Other social problems in U.S. society heighten the impact of barriers to health care access; among these problems, homelessness is of great significance. Despite their poverty, homeless people experience difficulty in obtaining needed care under public insurance programs. For instance, many programs require an address to ensure that the expenses of care are assigned to the correct county or other governmental unit. Because they may not be able to provide an address, the homeless frequently cannot obtain public coverage. In addition, they tend to be more vulnerable to access barriers even when covered.

· A 38-year-old uninsured, homeless man was admitted to a university hospital from the emergency room because of active pulmonary tuberculosis. He had come to the emergency room because of hemoptysis. During a week of hospitalization, including 2 days in the medical intensive care unit because of respiratory insufficiency, he was treated with three antibiotics, until his sputum was free of organisms. Due to financial problems, the hospital recently had initiated a policy that outpatient prescriptions would not be filled unless they were paid for directly by the patient or were chargeable to public or private insurance. For this reason, the patient was asked to travel after discharge to the county health department for his outpatient prescriptions to continue necessary treatment for tuberculosis. However, the patient did not find transportation and consequently did not receive his outpatient medications. Four weeks later, he again developed bloody sputum and respiratory distress, and was readmitted to the intensive care unit for active tuberculosis; this time, his treatment became more complicated since he had developed a medication-resistant organism because of the interruption in antibiotics.

Undocumented Immigrants

Another patient group experiencing major barriers to access is undocumented immigrants, who are not covered under most public programs. These individuals contribute substantially to the economic productivity of the United States, especially in the Southwest and Southeast regions, and pay much more in taxes than they receive in public benefits (5). Although they tend to be healthier and to utilize health care services less than age-matched U.S. citizens (6), they have few options for care when ill.

· A 31-year-old undocumented man from Mexico presented with carpal tunnel syndrome of his right hand, interfering with his work as a tailor. He had worked and had taxes deducted from his pay at a local clothing factory for the past 18 years. Acromegaly associated with a pituitary tumor was diagnosed, but radiation therapy or neurosurgery could not be arranged because of financial impediments. After waiting nearly 3 months for care, the patient was lost to follow-up when he returned to Mexico.

· A 22-year-old undocumented woman from Mexico with systemic lupus erythematosus was admitted to the intensive care unit because of delirium associated with end-stage renal failure and, after emergency dialysis, was stabilized. Hospital administrators decided not to permit long-term dialysis because of an anticipated cost of about $100,000 per year and the patient's lack of insurance. As a result, she was discharged from the hospital. Two weeks later she died at home.

The Working Poor

The following two patients show the special problems of working people who lose their insurance because of job loss. They also illustrate issues that are especially important for work in health services research and policy, described below.

· A 55-year-old man who served as office worker in a small horticultural company lost his job after 25 years with the same firm. One month later, he lost his health insurance, which had been provided as a fringe benefit of employment. After another month, he suddenly passed out and was taken to a county hospital's intensive care unit because his private physician refused to see him without insurance. Upper gastrointestinal hemorrhage from a bleeding duodenal ulcer, with resulting loss of consciousness, was diagnosed. After treatment with transfusions and medications, the patient slowly recovered. Nearly 1 year after losing his job, the patient found employment again as an office worker, received insurance coverage, and returned to his former physician for care.

· A 53-year-old woman, who had worked as a receptionist and clerical worker, was not working partly because of symptoms of pain and limited mobility associated with premature osteoporosis. She relied on the insurance coverage of her husband. About 3 months after he lost his job, she fell and fractured her forearm and wrist. Her private physician would not see her, due to lack of insurance coverage. She was taken to the county hospital, where resident physicians tried to realign the fractures, but she was left with a deformity.

These last two patients have been particularly influential for one of us (HW), as they were his parents. These individuals were proud people, who worked hard throughout their lives and were very reluctant to avail themselves of public welfare or insurance programs. As such, they viewed their problems as their own responsibility. At various times, they expressed the view that they somehow deserved the misfortunes that befell them, because they had not found a way to attend college during and after the Great Depression.

These cases illustrate two central themes regarding barriers to health care access in the United States. First, these barriers involve fundamental issues of personal dignity. The difficulties faced by each of these fellow humans degrade the individuals and families involved, at a time when they are most in need. Personal dignity requires more from social policy than we have yet achieved in the United States.

Second, such problems can happen to anyone, largely as a matter of bad luck. Severe illness, often requiring access to critical care medicine, can strike people who have lived their lives in accord with the mainstream standards of their communities. When misfortune arises, the United States does not provide a “safety net” ensuring access to basic medical services. Further, these problems do not only affect poor people and members of minority groups, although their impact is particularly severe for such individuals and families. Indeed, the barriers alluded to above—and detailed below—can exert unpredictable and devastating effects for a large part of the U.S. population, including a substantial part of the middle class.

The National Problems of Access and Costs

Having described barriers to access at the level of individual, flesh-and-blood patients who suffer from these problems, we now turn to the national level. The United States remains the only economically developed country in the world without a national health program that ensures universal access to health care services. Barriers to access and escalating costs of care have created a chronic crisis, which will continue as a target of policy during coming years.

Access

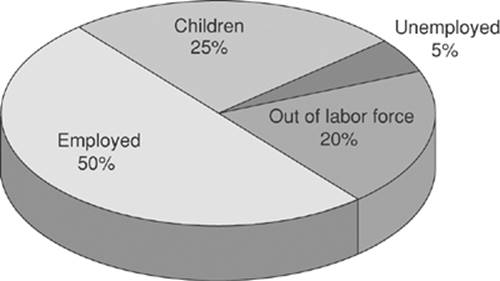

As of 2005, approximately 47 million people in the United States lacked health insurance (3). This number, representing about 16% of the population, has increased by more than 13 million persons during the past decade; most of the uninsured are working people (Fig. 1.2). Uninsured workers are spread across company size, as both large and small businesses frequently do not pay for health insurance as a fringe benefit of employment.

In addition to the uninsured, approximately 50 million people are underinsured (7). These are persons who, even though they hold health insurance policies, would be bankrupted by a major illness. Indeed, illness is currently the most frequent cause of personal bankruptcy in the United States (8). The underinsured include many elderly people, as well as a substantial part of the so-called middle class. For instance, Medicare pays for less than half of the medical expenses of senior citizens 65 years of age or older, and elderly people spend more money out of pocket on health care, in inflation-controlled dollars, than they did before the enactment of Medicare in 1965 (7). Many more millions of people cannot use their insurance because of copayments, deductibles, exclusions, or pre-existing medical conditions that disqualify them from coverage. U.S. private insurance ironically excludes those who need it most: People with pre-existing illness.

|

|

|

Figure 1.2. Who are the uninsured? Out of labor force = students older than 18 years, homemakers, the disabled, and early retirees. Source: Himmelstein DU, Woolhandler S. Available at: www.pnhp.org. Accessed March 15, 2007. |

|

|

|

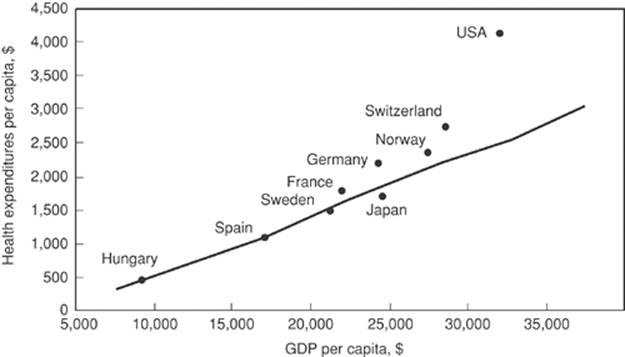

Figure 1.3. Health expenditures and gross domestic product (GDP) per capita, 1998. Source: Bodenheimer T. High and rising health care costs. Part 1: seeking an explanation. Ann Intern Med. 2005;142:84. |

Public programs do not adequately protect people who experience such barriers. For example, the national Medicaid program, which was initiated to provide needed care for poor people, has proven insufficient and has deteriorated over time. States have varied widely in the proportion of the population below the poverty level who are covered by Medicaid, and on average the proportion of the poor population eligible for Medicaid benefits has declined markedly since 1980. Indeed, our own experience at public, state-supported teaching hospitals suggests that some states work very hard not to pay for the services their citizens need. For example, at the University of Florida Health Science Center, patients from southern Georgia—often covered by Georgia Medicaid—are cared for. Interestingly, the state of Georgia Medicaid office often will not only not pay for the services provided their citizens, but also will not take calls from the Faculty Group Practice—the billing arm of the medical school—to determine what needs be done so payment from Georgia will be made. Caught in the middle, as one might expect, are the children of Georgia whose medical care is provided by University of Florida physicians, and whose expenses are covered by Georgia Medicaid.

Costs

In spite of these access problems, the costs of health care in the United States have continued to grow. Uncontrolled costs have become the second major component of the nation's health crisis. In 2005, these costs totaled more than $2 trillion annual, or about 16% of the gross national product (9). Between 1985 and 1992, health spending grew exponentially, despite explicit policies to control costs, including the expansion of managed care, the initiation of Medicare's program of diagnosis-related groups, and the spread of mandated utilization review. Although costs to corporations that purchased health insurance for employees moderated during the mid-1990s, these costs began to increase again during the late 1990s; costs for consumers continued to rise, as corporate employers passed on a greater proportion of their costs to employees (10).

The costs of health care in the United States far exceed those of any other country. For instance, on both an absolute and per capita basis, the United States spends much more on health care than any of the economically developed nations of Europe, Canada, and Japan (Fig. 1.3). All these other countries, despite their lower health care costs, have initiated national health programs that provide universal access to needed services (11).

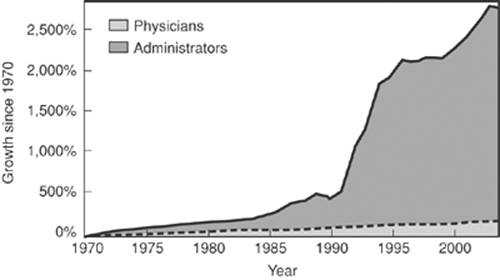

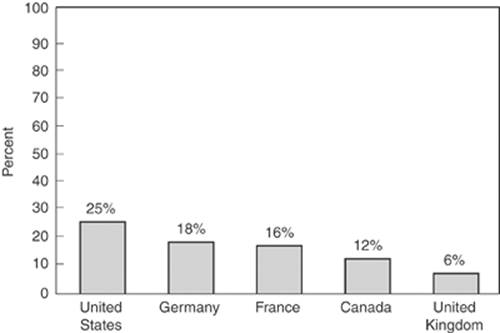

Although uncontrolled costs comprise a multifaceted problem, administrative waste deserves special emphasis (12). Figure 1.4 shows the growth of physicians and administrators in the U.S. health care system since 1970. As can be seen, administrators represent the fastest-growing sector of the health care labor force, expanding at three times the rate of physicians and other clinical personnel. The United States spends more on administration than any other economically developed country, with approximately 25% of health care costs going to this area. This figure compares unfavorably to all countries with national health programs, which spend between 6% and 14% of health care costs on administration (Fig. 1.5). If the United States could reduce administrative spending to a proportion comparable to that of countries with national health programs, the savings—currently about 10% of total expenditures of $2 trillion, or about $200 billion—would be adequate to provide universal access to health services without additional spending (9,13).

|

|

|

Figure 1.4. Growth of physicians and administrators, 1970–2004. Source: Himmelstein DU, Woolhandler S. Available at: www.pnhp.org. Accessed March 15, 2007. |

|

|

|

Figure 1.5. Administrative expenses as a percentage of all health care. Source: Waitzkin H. At the Front Lines of Medicine: How the Health Care System Alienates Doctors and Mistreats Patients…And What We Can Do About It. Lanham, MD: Rowman and Littlefield; 2004. |

|

|

|

Figure 1.6. A nurse suffering from a hospital-acquired infection Source: Waitzkin H. At the Front Lines of Medicine: How the Health Care System Alienates Doctors and Mistreats Patients…And What We Can Do About It. Lanham, MD: Rowman and Littlefield; 2004. |

How might administrative savings be achieved to help control costs? To answer this question, let us discuss the intensive care unit nurse shown in Figure 1.6. As judged by the spots on her uniform, this nurse suffers from a common hospital-acquired infection: “billing sticker-itis.” These stickers come from the sources shown in Figure 1.7. In most U.S. hospitals, each intravenous line, each medication, each gown, each surgical instrument, and each toothbrush has a billing sticker attached to it. A typical nurse like this one spends between 10% and 30% of his or her time gathering these stickers and on related administrative functions. The billing stickers are converted to cards or other pieces of paper and sent to the hospital's billing department, where—in a typical urban hospital—more than 100 employees computerize the charges and prepare separate bills for the more than 1,000 insurance companies that process private and public insurance claims. These companies differ widely in their reporting requirements, billing procedures, copayments, deductibles, exclusions, and other policies. Such different provisions greatly increase the administrative costs of submitting bills by hospitals and practitioners.

|

|

|

Figure 1.7. Source of the nurse's hospital-acquired infection, “billing sticker-itis.” Source: Waitzkin H. At the Front Lines of Medicine: How the Health Care System Alienates Doctors and Mistreats Patients…And What We Can Do About It. Lanham, MD: Rowman and Littlefield; 2004. |

A national health program in the United States could drastically reduce such wasteful administrative practices by eliminating the need for billing in hospitals. As in Canada and several European countries, hospitals could be funded through global annual budgets negotiated with the national health program, rather than the present costly and cumbersome billing apparatus. From the standpoint of insurance companies, administrative overhead comprises a rapidly growing component of costs. Overall, insurance overhead has increased to 11.7%, as compared to about 1.3% in Canada (12).

An additional component of administrative waste arises from the intense marketing and advertising of medical products. U.S. pharmaceutical and supply firms annually spend more than $10 billion on advertising and “detailing” of drugs and other medical products; this figure exceeds the total costs for teaching medical students in the United States. Such promotional activities are intended to influence physicians' prescribing habits. Patients and/or insurers bear the costs of these promotional activities through higher than necessary drug prices. Again, such wasteful practices could be restricted under a national health program that would provide needed medications and supplies, but at a lower overall cost.

In summary, we face a cruel contradiction in the United States. On the one hand, at least a third of our population face barriers to health care access because of lack of insurance, underinsurance, or insurance that cannot be used to meet existing needs. On the other hand, we spend more money on health care than any other economically developed nation, and the costs of care continue to rise at a rate that threatens our economic security. Paradoxically, the numbers of uninsured in the United States have increased roughly in parallel to increases in spending.

The Failure of Past Policies

At the heart of the health policy debate in the United States has been a very basic question: Is health care a basic human right, one that each of our citizens should have simply because they are citizens? Or should health care be treated like other commodities, such as cars, houses, and food—if one has the resources, one can obtain them; otherwise, one cannot? On the individual level is the issue of the inherent value of each person, and whether that value entitles one to health care. The concept of a right to needed services is not new to this country. For example, the constitutional right to legal representation guarantees that all individuals are entitled to basic services. However, the U.S. Constitution does not provide for a clear right to health care, in contrast to the constitutions of many other countries (14).

Policy Options

Competitive Strategies

Since the 1980s, competitive strategies have achieved prominence in health policy circles. Such proposals aim to foster competition among providers, and thus to lower costs (15). Competitive strategies culminated in “managed competition,” a policy option favored initially by the Clinton Administration (1992–2000) and whose elements appear in many recent proposals for a national health program. The basic assumption is that, by allowing competitive forces of the market to control health care delivery, competitive policies would result in a high-quality, cost-effective system.

Competitive strategies have received major criticism. Forces of competition generally have not controlled health care costs, as illustrated by the rise in overall costs at a rate higher than general inflation and by higher costs in regions with greater competition among health care providers (16). Further, medical services have never shown the characteristics of a competitive market, since government pays for more than 40% of health care, and the insurance, pharmaceutical, and medical equipment industries all manifest monopolistic tendencies that inhibit competition. Hospitals and physicians maintain political–economic power through professional organizations that reduce the impact of competitive strategies. Physicians also affect the demand for services through recommendations about referrals, diagnostic studies, and treatment. Analytically, the effects of competition on costs are difficult to separate from other important changes, especially the effects of general inflation, the requirement of major copayments by patients, and the impact of prepayment. Additionally, competitive strategies do not curtail administrative waste, as noted above.

Such competitive strategies in public programs also have led to major dislocations and gaps in services (17). For example, competitive contracting and prospective reimbursement under Medicaid have worsened the financial crises of hospitals with a large proportion of indigent clients. The resultant disruption in services due to underfunding of Medicaid has led to a measurable worsening of some patients' medical conditions. In some states, competitive health plans have suffered severe and unpredicted financial problems, and patients have encountered major barriers to access, including direct refusal of care by providers.

Several ethical issues have also arisen with competitive strategies. On an individual level, autonomy may be compromised through elimination of a patient's free choice of physicians and hospitals. Increased out-of-pocket costs may further impair autonomy by restricting access to care, especially among the poor. A multitiered system remains in place, as the working poor and unemployed receive more limited coverage than the middle class, who receive care different from that received by the wealthy and our national elected officials.

Corporate Involvement in Health Care

Various policies have encouraged corporate expansion in the medical field. By the mid-1970s, private insurance companies, pharmaceutical firms, and medical equipment manufacturers had already achieved prominent positions in the medical marketplace. In the 1980s and 1990s, multinational corporations took over community hospitals in all regions of the country, acquired and/or managed many public hospitals, bought or built teaching hospitals affiliated with medical schools, and gained control of ambulatory care organizations (18).

Corporate profitability in health care has encountered few obstacles, despite declines in profit margins for some corporations during the late 1990s. For instance, in 2006, profits as a percentage of revenues for the seven largest pharmaceutical corporations were between 14% and 21%—the highest among U.S. industrial groups (19). Nationally, for-profit chains came to control about 15% of all hospitals, but in some states—for example, California, Florida, Tennessee, and Texas—the chains operate between one third and one half of hospitals. Ownership of nursing homes by corporate chains has increased by more than 30%. For-profit corporations have enrolled over 70% of all HMO subscribers throughout the country.

While proponents perceive several economic advantages of corporate involvement in health care, substantiation of such claims is limited. For example, it is argued that tough-minded managerial techniques increase efficiency, enhance quality, and decrease costs, although several studies have shown that for-profit health care organizations perform worse or no better on these criteria than nonprofit ones (20). Similarly, research on corporate management has not supported the claim that corporate takeover can alleviate the financial problems of hospitals serving indigent clients (7).

Corporate involvement in health care has also raised ethical questions. For instance, there is concern that corporate strategies lead to reduced services for the poor. While some corporations have established endowments for indigent care, the ability of such funds to ensure long-term access is doubtful, especially when cutbacks occur in public-sector support. Other ethical concerns have focused on physicians' conflicting loyalties to patients versus their corporate employers, the implications of physicians' referrals of patients for services to corporations in which the physicians hold financial interests, and the unwillingness of for-profit hospitals to provide unprofitable, but needed, services, such as trauma programs. Such observations lead to doubts about the wisdom of policies that encourage corporate penetration of health care.

Public-sector Programs

Policies enacted since 1980 have greatly reduced public-sector health programs. Cutbacks have occurred in the Medicaid and Medicare programs, block grants for maternal and child health, migrant health services, community health centers, birth control services, health planning, educational assistance for medical students and residents (affecting especially minority recruitment), the National Health Service Corps, the Indian Health Service, and the National Institute of Occupational Safety and Health. Many federally sponsored research programs have also been cut. During this same time period, some measures of health and well-being in the United States either stopped improving or actually became worse. For example, a marked slowing in the rate of decline in infant mortality coincided with cutbacks in federal prenatal and perinatal programs; indeed, in several low-income urban areas, infant mortality increased. Among African Americans, postneonatal and maternal mortality rates stopped falling after decades of steady decline, many African American women did not receive adequate prenatal care, and overall mortality rates for African Americans, especially men, remained much worse than those for Caucasians (7). These reversals in health status and health services, emerging as direct manifestations of changes in federal policies, have been unique among economically developed countries.

Alongside these programmatic cutbacks, bureaucratization and regulation in the health care system have grown rapidly. A distinction between the rhetoric of reduced government, versus the reality of greater government intervention, is nowhere clearer than in the Medicare diagnosis-related group (DRG) program. Intended as a cost-control device, DRGs introduced unprecedented complexity and bureaucratic regulation. By providing reimbursement to hospitals at a fixed rate for specific diagnoses, DRGs encouraged hospitals to limit the length of stay, as well as services provided during hospitalization. Hospitals responded to DRG regulations with an expansion of their own bureaucratic staffs and data-processing operations, more intensive utilization review, and a tendency to discharge patients with unstable conditions. Private hospitals admitting a small proportion of indigent patients profited under DRGs; public and university hospitals that served a higher percentage of indigent and multiproblem patients faced an unfavorable case mix within specific DRGs and, thus, fared poorly. The extensive utilization review that DRGs encouraged focused on cost cutting, rather than ensuring quality of care. Moreover, DRGs' contribution to cost control remained unclear, in comparison to other factors such as reduced inflation in the economy as a whole.

The Place of Critical Care Medicine in a Health System

Any health system, however organized, will have need for subspecialty care, including critical care medicine services. Even in a system in which primary and preventive services are emphasized, there will be traumatic injuries, perforated colons, and massive hemorrhages resultant from surgical interventions, all requiring intensive care services. In the United States 27% of Medicare spending is for end-of-life care, and 46% of all Medicare charges occur in the last year of life, most in the last 60 days of life (21,22). This is a significant portion of national health spending—encompassing about $91 billion in 2001 (0.9% of the gross domestic product) (23)—and one might ask if there is value generated by this spending.

While, in general, life-saving therapy costing less than or equal to US $100,000 per quality adjusted life year (QALY) saved is considered “cost effective” (i.e., is of “value”), there are some technical problems with this method of determining usefulness, or cost effectiveness of different therapies. For example, QALY is a mathematically derived value of the health-related quality of life during a given time period during which survival has occurred. One QALY may not be equal to another and, in fact, it has been suggested that this is not the case (24). When considering terminally or critically ill patients, cost per QALY may not be useful for several reasons: (a) in physician–patient interactions, decisions are not frequently made based on this parameter; (b) data and methodologic uncertainties inherent in the generation of this metric are not easily handled, making the analysis appear mathematically rigorous when it is in fact not; and (c) the metric does not answer the question of how one treatment compares with another (24).

Finally, although palliative care—as appropriate—has been suggested as a means to decrease the use of health resources, including use of critical care services, it appears that this would impact only about 10% of spending during the last year of life (22).

Thus, for better or for ill, in the system of care in the United States, 33% to 50% of individuals spend time in an intensive care unit (ICU) during their last year of life. Approximately 20% of those who die do so in an ICU. The use of ICU services incurs significant costs of between approximately $2,000 and $3,000 per day; this is about sixfold higher than a non-ICU day. Although the ICU accounts for only 8% of total hospital beds, 20% of hospital expenditures are incurred while patients are in the ICU (23,25). While these numbers apply to the United States, other industrialized countries have similar issues, although ICUs may represent, in these countries, a smaller portion of the health system.

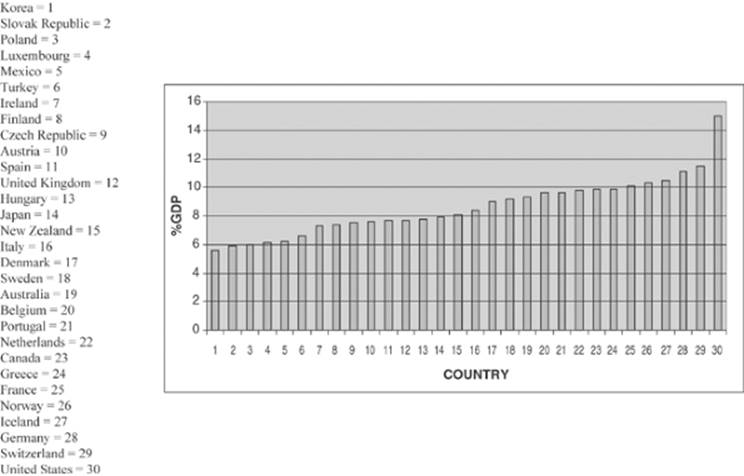

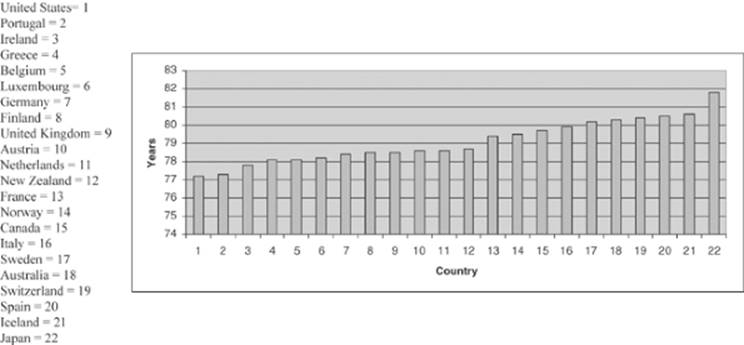

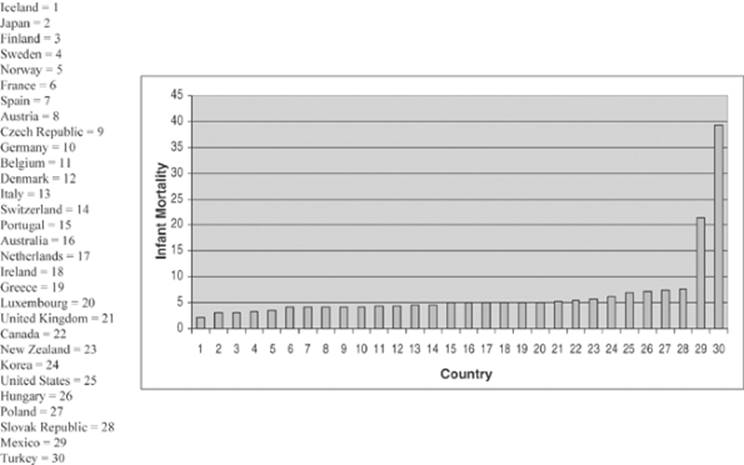

So if in any health system, no matter whether organized under capitalist (United States), social democratic (Norway), or socialist (Cuba) principles, ICUs will make up a component of the system, at least part of the duty of those in charge of these units must be to ensure that the social resources are efficiently utilized (23,25). Table 1.2 details some of the techniques that may be put in place in an attempt to ensure the quality of ICU services. And how might we define quality? Simply put, the services provided are those that are needed; they are provided humanely; the services follow—at minimum—best practice, evidence-based medicine; the services utilized are provided with technical excellence; and, finally, the principle of the “commons”—that these resources are social and that they need be distributed with fairness—is observed. The fact that the health system of the United States is the most expensive of the industrialized countries, while ranking 37th in performance and 72nd in population health, is suggestive of what we ought to try to change (23). Figures 1.8, 1.9 and 1.10 detail some of this information.

|

Table 1.2 Parameters Enhancing Quality of Intensive Care Unit (ICU) Care |

||

|

Where to from Here?

With increasing discontent among the general public and practitioners, health policy debates have taken on a certain urgency. While an ethical perspective tells us that basic health care for all is an individual right and a societal obligation, the burgeoning costs of the U.S. system hamper domestic economic growth and stability, and meanwhile, millions of people face major access barriers. Is there a better way to handle this problem? What are some of the models from which we might draw inspiration?

Change in health policies to address these problems doubtless will occur, but the specifics of change remain difficult to predict in the complex political terrain of the United States. The last part of this chapter examines local and national actions to correct the difficult problems of access and costs. There is no justification for the continuing and needless suffering experienced by human beings such as those whose stories are summarized earlier in this chapter. In this rich and powerful country, we deserve better.

Perspectives from Other Countries

Planning for a national health program in the United States requires open-minded consideration of the strengths and weaknesses of presently existing national health programs around the world. For instance, most countries in Western Europe and the Scandinavian area have initiated national health program structures, permitting private practice in addition to a strong public sector. Canada has achieved universal entitlement to health care through a national health program that depends on private practitioners, private hospitals, and strong planning and coordinating roles for the national and provincial governments. Thus, we must not condemn ourselves to the fallacy that thinking and planning for a national health care system must, by definition, remove some of what is most loved about our health system today: The intimate, one-on-one personal interaction between physician and patient.

National health programs vary widely in the degree to which the national government employs health professionals and owns health institutions. For example, the national health programs of the United Kingdom, Denmark, and the Netherlands1 contract with self-employed general practitioners for primary care; Canadian private practitioners receive public insurance payments on a mainly fee-for-service basis; and in Finland and Sweden a high proportion of practicing doctors work as salaried employees of government agencies. In the United Kingdom, the national government owns most hospitals; regional or local governments own many hospitals in Sweden, Finland, and other Scandinavian countries; and Canada's system depends on governmental budgeting for both public and private hospitals.

|

|

|

Figure 1.8. Percent gross domestic product (GDP) expended on health—world—2003. Source: www.irdes.fr/ecosante/OCDE/500.html. |

|

|

|

Figure 1.9. Life expectancy at birth—world. Source: www.irdes.fr/ecosante/OCDE/111000.html. |

The Canadian system is very pertinent to the United States, because of geographic proximity and cultural similarity. Canada ensures universal entitlement to health services through a combination of national and provincial insurance programs. Doctors generally receive public insurance payments on a fee-for-service arrangement. Hospitals obtain public funds through prospectively negotiated contracts, eliminating the need to bill for specific services. Progressive taxation finances the Canadian system, and the private insurance industry does not play a major role in the program's administration. Most Canadian provinces have initiated policies that aim to correct remaining problems of access based on geographic maldistribution. Cost controls in Canada depend on contracted global budgeting with hospitals, limitations on reimbursements to practitioners—a policy that remains controversial for physicians in some provinces—and markedly lower administrative expenses because of reduced eligibility, billing, and collection procedures.

|

|

|

Figure 1.10. Infant mortality: Deaths per 1,000 live births—world—2002. Source: ww.irdes.fr/ecosante/OCDE/500.html. |

Because of the commonly expressed concern about costs in the United States, the experiences of existing national health programs are instructive. U.S. health care expenditures, already the highest in the world, account for approximately 16% of the gross domestic product. The presumption that a national health program would increase costs is not necessarily correct; depending on how it is organized, costs might well fall to below their prior level. First, a major savings would come from reduced administrative overhead for billing, collection procedures, eligibility determinations, and other bureaucratic functions that no longer would be necessary. In the Canadian national health program, for instance, global budgeting for hospitals has greatly reduced administrative costs, and a much smaller role for the private insurance industry has lowered costs even further by restricting corporate profit. A classic but still accurate analysis by the U.S. General Accounting Office showed that, due to savings from reduced administrative functions and entrepreneurialism, a single-payer national health program like Canada's, if introduced in the United States, would lead to negligible added costs despite achieving universal access to care (13).

A National Health Program for the United States

Because of the deepening crisis created by the problems of access and costs, both locally and nationally, a national health program for the United States has cycled on and off the policy agenda for many years. Unsuccessful proposals for such a program span three quarters of a century of U.S. history (26), so the pace of passage and implementation remains in doubt. During the first years of the Clinton Administration, another cycle of intense debate occurred, but proposals again suffered defeat. As a result, the United States remains the only economically developed country without a national health program that provides universal entitlement to health care services. Yet because the underlying problems of access and costs have persisted, and have actually continued to worsen in many respects, the need for a national health program still remains recognized by broad segments of the U.S. population.

Although policy debates change quickly and often focus on much more limited reforms, two options have remained as the most prominent proposals for a national program: Those based on managed care versus those based on a “single-payer” system modeled broadly along the lines of Canada's national health program. At the outset, we wish to make clear that one of us (HW) helped develop the single-payer proposal, and that the following discussion favors the single-payer approach (27). While taking a more critical view of managed care as an organizing principle for a U.S. national health program, the references include defenses of this approach, which can be reviewed to obtain more information about the proponents' views.

Principles and Prospects for a U.S. National Health Program

National health program proposals can be appraised against several basic principles:

· The national health program would provide for comprehensive care, including diagnostic, therapeutic, preventive, rehabilitative, environmental, and occupational health services; dental and eye care; transportation to medical facilities; social work; and counseling.

· These services generally would not require out-of-pocket payments at the “point of delivery.” While carefully limited copayments for certain services may be appropriate—as is done in Canada—the careful, thoughtful, and appropriate implementation of copayments would ensure that they do not become barriers to access.

· Coverage would be portable, so that travel or relocation has no effect on a person's ability to obtain health care.

· Financing for the national health program would come from a variety of sources, including continued corporate taxation, “health taxes” on cigarettes and alcoholic beverages, “conservation taxes” on fossil fuels and other energy sources, “pollution taxes” on known sources of air and water pollution, and a restructured individual tax. Taxation would be progressive, in that individuals and corporations with higher incomes would pay taxes at a higher rate.

· The national health program would reduce administrative costs, private profit, and wasteful procedures in the health care system. A national commission would establish a generic formulary of approved drugs, devices, equipment, and supplies. A national trust fund would disburse payments to private and public health facilities through global and prospective budgeting. Profit to private insurance companies and other corporations would be closely restricted.

· Professional associations would negotiate the fee structures for health care practitioners regionally. Financial incentives would encourage cost-control measures through health maintenance organizations, community health centers, and a plurality of practice settings.

· To improve geographic maldistribution of health professionals, the national health program would subsidize education and training in return for required periods of service by medical graduates in underserved areas.

· The national health program would initiate programs of prevention that emphasize individual responsibility for health, risk reduction—including programs to reduce smoking, alcoholism, and substance abuse—nutrition, maternal and infant care, occupational and environmental health, long-term services for the elderly, and other efforts to promote health.

· Elected community representatives would work with providers' groups in local advisory councils. These councils would participate in quality assurance efforts, planning, and feedback that would encourage responsiveness to local needs.

· The central democratic and representative principle that decisions—local, regional, and national—about health system financing priorities, and delivery decisions, would be made by the “three-legged stool” approach; namely, the government, practitioners, and patients would all be involved in the debate and decision making, as a matter of law.

There is and has been wide support for a national health program in the United States. Public opinion polls have shown that a majority of the U.S. population favors a national policy that ensures universal entitlement to basic health care services. Professional organizations including the American Medical Association,2 the American College of Physicians, the American Public Health Association, the American College of Surgeons,3 and Physicians for a National Health Program—a major physicians' organization favoring a single-payer option—have called for a national health program. Leaders and members of corporations, senior citizens' groups, and a large number of civic organizations have pressed Congress to create a national health program, although the specific proposals have varied. Likewise, many state legislatures have considered setting up state health programs to provide universal access to care.

Strong opposition to a national health program will continue to come from the corporations that currently benefit from the lack of an appropriate national policy: The private insurance industry, pharmaceutical and medical equipment firms, and the for-profit health care chains. While corporate resistance should not be underestimated, there is also support for a national health program from the corporate world. The costs of private sector medicine have become a major burden to many nonmedical companies that provide health insurance as a fringe benefit to employees. Corporations that do not directly profit from health care have influenced public policy in the direction of cost containment. In Canada, Western Europe, and Scandinavia, corporations have come to look kindly on the cost controls and services that national health programs provide, even when corporate taxation contributes to the programs' financing.

A National Health Program Based on Managed Care

Proposals for managed care as the basis of a national health program have been complex and have changed over time. The Clinton Administration presented a lengthy proposal that received wide attention during the mid-1990s but was ultimately defeated by a broad coalition of interest groups. Although Clinton did not pursue this proposal in the later years of his presidency, its framework has remained the basis of other proposals, and the managed care approach likely will persist in future proposals. For instance, elements of the managed care approach appeared in the proposals of candidates entering the 2008 presidential campaign. Our purpose here is to summarize the key features of managed care as the central principle of a national health program and some of the concerns that have been raised about this approach.

Managed care, although difficult to define simply since it encompasses diverse organizational structures, generally refers to administrative control over the organization and practice of health services, through large corporate entities. Historically, managed care has included such prepaid approaches as HMOs, preferred provider organizations (PPOs), and proposals for national programs organized on principles of administrative control and market competition. Managed care assumes that quality of care is ensured through administrative control and through competition in the marketplace.

The first proposals for a national health program based on managed care appeared during the 1970s. In 1977, Alain Enthoven, an economist whose prior career had focused on military policy analysis at the U.S. Department of Defense and corporations serving as military contractors, offered to the Carter Administration a proposal for a “Consumer Choice Health Plan,” based on “regulated competition in the private sector.” This proposal was built in part on prior initiatives by Paul Ellwood for a national “health maintenance strategy” and by Scott Fleming for “structured competition within the private sector” (28). Although Carter rejected the plan, Enthoven soon afterward published the proposal in the medical literature (29) and in a separate monograph (30). This plan, which presented the basic conceptual structure of all subsequent proposals for national health programs based on managed care, contained important concepts from the military policy work that Enthoven had spearheaded a few years earlier at the Pentagon (31).

During the 1980s, Enthoven collaborated with Ellwood, other proponents of HMOs, corporate executives, and officers of private insurance companies in developing refinements of the proposal. An emphasis on “managed competition” arose during the mid-1980s, in response to concerns raised by economists and business leaders that the original proposal conveyed free-market assumptions requiring modification through closer “management” of the program (32). After publication of a revised proposal in 1989 (33), the coalition supporting managed competition broadened to include officials of the largest U.S. private insurance companies that were diversifying into managed care. These business leaders entered into continuing meetings with Enthoven and other proponents of managed competition at Ellwood's Wyoming home, as part of the so-called “Jackson Hole group.” The managed care sector of the private insurance industry provided major funding for the Jackson Hole group, as well as financial and logistic support for the Clinton presidential campaign and consultation for the Presidential Health Care Task Force.

Although most proposals for managed competition have emerged from this intellectual tradition, certain proposals have suggested modifications in the conceptual structure outlined by Enthoven and colleagues. For instance, although managed competition traditionally has encouraged employer-sponsored plans with participation by private insurance companies, other proposals have separated employment from insurance through the creation of a single, tax-financed, globally budgeted public fund, which would contract with private plans for a minimum benefit package (34). All managed competition proposals, however, incorporate concepts initiated by Enthoven and colleagues, and all of them call for large-scale changes in how professionals practice medicine, and how physicians and consumers make choices.

There are four essential features of managed competition. The first element involves large organizations of health care providers. As described in the Clinton proposal, these “accountable health partnerships” (AHPs) are large, integrated organizations of insurers and providers that would offer health plans competitively. Large businesses would participate in these partnerships. The AHPs would operate much as do current managed care organizations (MCOs) and would drastically reduce medical practice based on fee-for-service reimbursement. Instead, physicians and hospitals would be largely absorbed into MCOs. In principle, this shift in the organization of medical practice would allow more stringent management of practice conditions by high-level managers, whose responsibility would be to control costly and potentially self-interested actions by physicians and hospitals.

A second major element of the proposal involves large organizations of purchasers. The Clinton proposal referred to these organizations as “health insurance purchasing cooperatives” (HPICs); similar proposals have used somewhat different terminology. Such organizational purchasers would buy health plans from the large organizations of health care providers (AHPs in the Clinton plan). Organized mainly by state governments, these large purchasers would represent small employers and individuals, including both self-employed and unemployed people. In theory, these large, “intelligent purchasers” would make informed decisions about costs and quality of services. Under managed competition, Medicaid and possibly Medicare eventually would be privatized and converted to sponsorship by state-organized purchasers.

A uniform benefits package, referred to as “uniform effective health benefits” (UEHBs) in the Clinton proposal, is the third essential component of a national health program based on managed care. This benefits package would be extended to the entire population. An appointed national health board would define the minimum benefits contained in the package. This board's decisions about coverage would rely mainly on research about the outcomes and effectiveness of health services.

Tax code changes comprise the fourth essential element of a national health program based on managed care. These changes would restrict the ability of corporations and individuals to claim tax deductions for health care expenditures. Specifically, corporations and individuals could not claim tax deductions for coverage that exceeds the basic coverage provided by the minimum benefits package. Although corporations and individuals could buy additional coverage without tax deductions, these changes in tax code would provide incentives to purchase less expensive coverage overall.

Advocates of a managed care approach to a national health program claim several advantages of this approach. First, it would expand access to health services while still preserving a major role for the private insurance industry. Insurance companies, for instance, could run large managed care programs as fundamental parts of AHPs. As a result, this approach would create less drastic changes in the U.S. health system than a single-payer plan and thus, proponents argue, would stand a better chance of passage in Congress. Because managed care would rely on market forces for cost containment, according to advocates, it would prove more consistent with mainstream political and economic values. Competition, from this view, would lead to improved quality, since managed care plans would have to compete with one another for patients. In selecting among competitive plans, consumers also would need to become more informed about cost-effective care, partly because they would be required to pay copayments for most services.

Several unknowns have persisted in such proposals, and the Congressional debate on the Clinton Administration proposal was unable to fully clarify these issues. The extent of the basic benefits to be covered under a national program remained to be worked out. Details of how a national program based on managed care would be financed, in particular the tax increases to be borne by families and corporations, were not clearly specified. This latter question about the specifics of projected tax code changes, of course, was important, since estimates of the additional costs of a national health program based on managed care ranged from $30 billion to $100 billion per year. Whether overall health care expenditures would be capped through a global budgeting mechanism remained ambiguous. How transition would occur from the present system was not clarified. Further, the degree to which state governments would enjoy flexibility to enact varying forms of coverage and organization remained under debate.

Both supporters and opponents have raised major concerns about managed care as the basis of a national health program. Demographic limitations would restrict its impact, since about 30% of the U.S. population live outside metropolitan areas that could support three or more competing managed care plans. Proponents of managed care have emphasized these demographic limitations to the success of a national health program based on managed care principles (35). Whether managed care could control costs remains unclear; states with the most extensive managed care programs have shown costs as high, or higher, than elsewhere. Administrative costs, already more than 25% of overall health care expenditures, likely would increase still further, since managed care is administratively intensive and new organizational sponsors would introduce additional managerial layers. Despite intent to use research on effectiveness and outcomes to define the uniform minimum benefits package and to assess quality of care, such research has produced verified data about only a small number of medical conditions and procedures.

Several practical questions also have arisen concerning acceptability of a national health program based on managed care to providers and consumers. While expanding the decision-making power of large insurance companies, such a program probably would reduce consumers' freedom to choose practitioners, and micromanagement of clinical decisions likely would increase. Because the ability to buy additional coverage beyond the basic benefits package would depend on income, this provision would perpetuate unequal, multitiered coverage. Whether a national program would succeed in curbing insurance companies' selection or exclusion of patients by risk of costly illness remains in doubt. Managed care likely would create higher out-of-pocket payments and taxes for a substantial part of the population who currently are insured. Furthermore, several polls have shown less public support for managed care as a basis for a national health program than for other alternatives. Evidence that managed care would solve the access problem while controlling costs remains uncertain. Importantly, it is not clear whether a national health program could address successfully the problems and tensions that managed care has introduced into the patient–doctor relationship.

Finally, the place of academic medicine, especially in the context of continuous and ongoing funding needed for education, research, and quality improvement, is unclear in this system.

We look to our system of university-based health science centers not just for scientific and technical advances, but for the creation of the next generation of practitioners: Physicians, nurses, respiratory therapists, occupational and physical therapists, laboratory technicians, and so forth. How will the alteration in funding impact the education of these individuals? How will the altered organization of health care affect the already precarious financial position of the academic medical center? Such questions remained unanswered under managed care proposals for a national health program.

The powerful coalition built up around managed care as the basis for a national program did not succeed in enacting this policy. Although it addressed some of the concerns raised about managed care, the Clinton team did not agree to change the basic structure of the proposal. This reluctance to consider other options seriously may have stemmed partly from the support that the Clinton campaign received from the managed care sector of the private insurance industry, as well as a perception that simpler and more popular options, including a single-payer approach, were unlikely to pass Congress.

Failure to achieve a workable national health program generated great disappointment, as well as financial waste. Some analysts believed that failure of managed care was a necessary step toward adoption of a simpler approach such as a single-payer option. A less sanguine view holds that the Clinton failure led to retrenchment, cutbacks, and reinforcement for the paradox of pervasive access barriers coupled with high costs.

A Single-payer National Health Program

This option would provide universal entitlement to needed health care while controlling costs through a single-payer financing system. A single-payer, or “monopsony,” financial structure has achieved substantial savings by reducing administrative waste in the national health programs of Canada, Sweden, and Australia. While none of these programs is without problems, all have minimized barriers to access while controlling costs.

The following features of a single-payer option are based on the proposals of Physicians for a National Health Program (PNHP), of which one of us (HW) is a founding member. The summary provided here leaves out details contained in national publications to which many colleagues have contributed (28,36,37,38). From its initiation in 1985, PNHP has grown as a national organization to include more than 13,000 members, who are physicians and other health professionals spanning all specialties, states, age groups, and practice settings. Participants in PNHP have come together with a common perception that the problems of access and costs are intolerable and a belief that a single-payer national health program will remove barriers to access while controlling costs. Although supported by a substantial proportion of the U.S. population in polls, a single-payer system was not the option proposed by the Clinton Administration. On the other hand, a single-payer approach did emerge as one of the two options for a national health program under consideration in the U.S. Congress.

|

|

|

Figure 1.11. Funding for a national health program (NHP) under the single-payer proposal. HMO, health maintenance organizations. |

Coverage under the single-payer proposal would be universal—everyone would be covered. The national health program would provide comprehensive coverage for all medically necessary care, including long-term care. Under this plan, there would be no out-of-pocket costs or copayments for needed services. Copayments are not preferred since they have been found to be substantial disincentives to needed care among low-income patients. Further, copayments would not be necessary because costs would be controlled by a single, publicly financed plan that would greatly curtail administrative waste and would achieve cost reductions through monopsony financing. A single-payer national health program would eliminate competing private insurance. This approach would facilitate cost control and would discourage multiple tiers of care for different income groups, but of course would engender opposition from the wealthy and powerful private insurance industry.

Under a single-payer national health program, hospitals would receive payment through a global budgeting system. The very costly billing apparatus, which is responsible for unnecessary administrative costs in hospitals under the present system, would be eliminated. Instead, hospitals would negotiate an annual global budget for all operating costs. It is important to note that hospitals would remain privately owned and run, rather than becoming part of a nationalized ownership structure. To reduce overlapping and duplicative facilities that increase overall costs, capital purchases and expansion would be budgeted separately, based on regional health planning goals. Regional health planning boards, with members elected by consumers and providers, would make these decisions about capital expenditures and expansion.

The national health program would collect and disburse virtually all payments for health services (Fig. 1.11). This single-payer structure would provide the major overall source of cost control. Total expenditures would be capped at the proportion of the gross domestic product spent for health services during the year prior to implementation of the national health program. Initially, during a transition period of approximately 3 years, funding would come from existing sources to minimize economic disruption: Medicare and Medicaid, state and local governments, employers, and private insurance premiums. After the transition period, the collection of payments would be converted to a simplified process based on taxation, in which the average company, individual, and family would pay approximately the same in taxes as was previously paid in insurance premiums, deductibles, copayments, and other out-of-pocket spending.4 The national health program would distribute payments for services to hospitals, MCOs, physicians, home care agencies, and long-term care agencies.

Payment for physicians and ambulatory care would occur under one of three options. First, physicians could choose to be paid on a fee-for-services basis. Under this option, state medical associations would negotiate a simplified fee schedule for the range of covered services; practitioners would accept fees as payment in full and would not bill patients separately, except for a small number of uncovered services such as purely cosmetic surgery. As a second option, the national health program would provide capitation payments to MCOs employing salaried physicians. However, provisions of this option would protect against possible abuses seen under prior managed care programs; for instance, free disenrollment privileges would be required, and MCOs would be prohibited from selective enrollment of healthier patients. Capitation fees would cover operating costs only, rather than capital purchases, profits, or physician incentives. Under the capitation option, global budgeting would apply to inpatient care. The third option for physician payment would involve salaries received from globally budgeted institutions, such as hospitals, community clinics, and home care agencies.

The national health program would cover all needed drugs and medical supplies. An expert board would develop a national formulary based on principles of generic drug substitution and assurance of high standards of biologic quality. As far as possible, reimbursement procedures would encourage the use of less expensive generic alternatives. This provision would reduce the excessive costs incurred from the promotion and detailing of new drugs without greater demonstrated efficacy than less expensive formulations.

How would the national health program look from the patient's point of view? First, universal access to comprehensive care would remove barriers to access. There would be no out-of-pocket costs, and patients would have free choice of doctors and hospitals. Hassles in using and processing private or public insurance would be reduced through the implementation of a single program for everyone.

From the practitioner's point of view, conditions of practice would improve considerably, especially because the wallet biopsy—that emotionally and ethically degrading procedure that physicians often must use before deciding how to diagnose or treat a patient—no longer would be necessary. Instead, the national health program would cover fully all needed services. Doctors would most likely experience greater clinical freedom and less intrusive micromanagement by administrators. In addition, physicians would be free to choose from a variety of practice settings. Overall, there would be little change in anticipated income; as in Canada, practitioners in the primary care specialties could anticipate equal or somewhat greater earnings than previously, and only the highest paid surgical subspecialists could expect to see a fall in income.

|

|

|

Figure 1.12. Cost of health insurance in a new car, by country of production. Source: Waitzkin H. At the Front Lines of Medicine: How the Health Care System Alienates Doctors and Mistreats Patients…And What We Can Do About It. Lanham, MD: Rowman and Littlefield; 2004. |

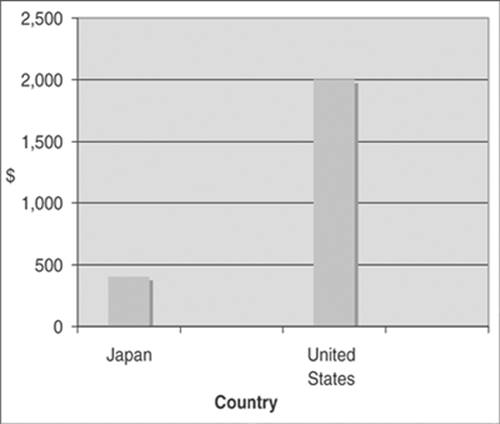

From the corporate viewpoint, companies would experience stabilization in costs of health care. Those corporations that currently provide health insurance as a fringe benefit of employment likely will see a reduction in health care expenses; projections for automobile manufacturers like Ford or Chrysler indicate that costs will decline more than $4,000 per employee per year. Companies that do not currently provide health insurance as a fringe benefit will experience higher costs, but the single-payer national health program will provide subsidies for small businesses that are at greatest financial risk. Economic competitiveness of U.S. corporations overall will increase, since companies will incur health care costs more in line with those of their international competitors. Figure 1.12 depicts the international disadvantage for U.S. automakers, which spend much more per car on health care than do their competitors in countries with national health programs.

In summary, a single-payer national health program would provide universal, comprehensive coverage, without out-of-pocket payments. Hospitals would be paid a global, “lump sum” operating budget, to be negotiated annually. Capital budgets for hospitals would be negotiated based on regional health planning goals. Physicians and ambulatory care would be paid through one of three options: Fee for service, capitation in HMOs, or salary in globally budgeted institutions. A single, public payer would control costs and achieve public accountability while minimizing administrative waste. Simplicity and international experience with the single-payer approach make it a reasonable alternative for a U.S. national health system, but rationality by no means guarantees political success.

Summary

The political process surrounding a national health program, as practiced in the United States, conveys an overall sense of irrationality and lack of coherent policy. This irrationality and incoherence become even more apparent from an overview of the comparative costs of various local and national policies. For instance, the cost of initiating a single-payer national health program that would solve the access problem while controlling costs would consume very little additional expenditures, certainly an order of magnitude less than current expenditures on possibly outdated or unnecessary military systems like the Stealth bomber, as well as public support of the private financial sector in such efforts as savings and loan bailouts. On the other hand, as estimated by the U.S. Congressional Budget Office, a national health program based on managed care would represent a substantial increase in expenditures, on the order of $80 billion per year (39).

For better or worse, the lack of a national health program will continue to plague the United States. Patients and practitioners, including those who specialize in critical care medicine, will continue to experience this unpleasant reality until we, as a country, finally correct the problem through concerted action. The chronic crisis of U.S. health policy gives reasons for pessimism but also clarifies some of the opportunities that await us in trying to construct a more humane society and a more humane health care system.

References

1. Congressional Budget Office. How Many People Lack Insurance and for How Long? Washington, DC: Congressional Budget Office; 2003.

2. DeNavas-Walt C, Proctor BD, Lee CH. U.S. Census Bureau: Current Population Reports. In: Income, Poverty, and Health Insurance Coverage in the United States: 2005. Washington, DC: U.S. Government Printing Office; 2006.

3. Davis K. Uninsured in America—problems and possible solutions. Br Med J. 2007;334:346.

4. American Medical Association. Ending the patient-physician relationship. Available at: http://www.ama-assn.org/ama/pub/category/4609.html. Accessed March 13, 2007.

5. Berk ML, Schur CL, Chavez LR, et al. Health care use among undocumented Latino immigrants. Health Aff (Millwood). 2000;19:51.

6. Goldman DP, Smith JP, Sood N. Immigrants and the cost of medical care. Health Aff (Millwood). 2006;25:17

7. Waitzkin H. At the Front Lines of Medicine: How the Health Care System Alienates Doctors and Mistreats Patients…And What We Can Do About It. Lanham, MD: Rowman and Littlefield; 2004.

8. Himmelstein DU, Warren E, Thorne D, et al. Illness and injury as contributors to bankruptcy. Health Aff (Millwood). 2005; Suppl Web Exclusives:W5-63-W5-73.

9. Centers for Medicare and Medicaid Services. National health expenditure data. Available at: http://www.cms.hhs.gov/NationalHealth ExpendData/02_NationalHealthAccountsHistorical.asp. Accessed March 31, 2007.

10. Kuttner R. The American health care system: health insurance coverage. N Engl J Med. 1999:340.

11. Bodenheimer T. High and rising health care costs. Part 1: seeking an explanation. Ann Intern Med. 2005;142:84.

12. Woolhandler S, Campbell T, Himmelstein DU. Costs of health care administration in the United States and Canada. N Engl J Med. 2003;349:768.

13. U.S. General Accounting Office. Canadian Health Insurance: Lessons for the United States. Washington, DC: Government Printing Office (GAO Publ. No. GAO/HRD-91-90; B-244081); 1991.